In the first installment of my Media Metrics series, I presented an analytical framework that can be used to evaluate the state the media marketplace and specific media sectors. I also argued that within each segment of the media value chain (Content options >> Distribution options >> Receiving options >> Storage options) we see more choice, competition, and diversity than ever before in human history. As this fifth installment of the series will show, nowhere is that fact more evident than in the market for audible information and entertainment, which has undergone radical transformation over the past decade.

For most of the past century, the audible information and entertainment sector was generally thought of as broadcast radio, the recorded music industry, and the live music business. It was a fairly stable industry that did not witness business model-shattering type changes. For radio, AM gave way to FM. For recorded music, vinyl gave way to tapes and CDs. And live music simply found larger (and more) venues.

Today, however, stability has given way to volatility. This entire marketplace is in a state of seeming constant upheaval. Everything has changed and continues to change at a rapid pace as “disruptive technologies†fly at us with increasingly regularity. Old business models are breaking down, and new ones are multiplying. Long-standing industry players are shedding assets or even disappearing as underdogs rapidly enter the sector and become big dogs overnight. You want a textbook example of Schumpeterian creative destruction in action? This market is it.

Exhibit 1

Let’s take a look at how competition and choice is shaping up. Note: I don’t think I need to spend much time here documenting the upheaval in the recorded music sector since it has been well-documented elsewhere. The recorded music business as we have known it is in serious trouble. Of course, part of that upheaval we see at work in that sector has been brought about by the breakdown of copyright more generally, which makes the analysis more complicated regarding whether or not change in that sector will benefit consumers in the long-run.

But creative destruction and marketplace evolution is clearly benefiting consumers overall. Consumers have more choices and more options than ever before.

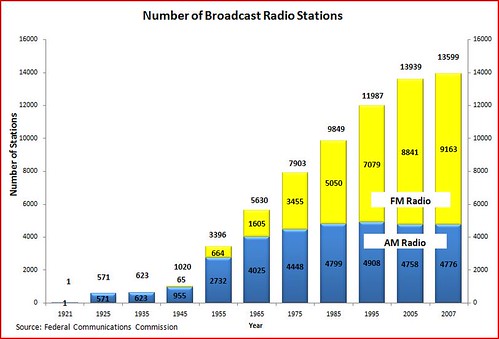

Terrestrial Broadcast Radio

Start with the oldest sector: terrestrial broadcast radio. There are more broadcast radio stations in America today than ever before. The number of broadcast radio stations has roughly doubled since 1975, from 7,903 stations in 1975 to 13,599 stations in 2007.

Exhibit 2

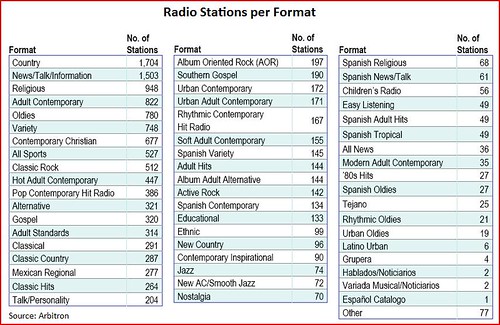

And, as Exhibit 3 shows, the number of radio formats has proliferated and is quite diverse.

Exhibit 3

Meanwhile, terrestrial radio operators are rapidly rolling out HD radio and online multicasts to offer local content in all new ways. And terrestrial radio remains the same price it always has been: free!

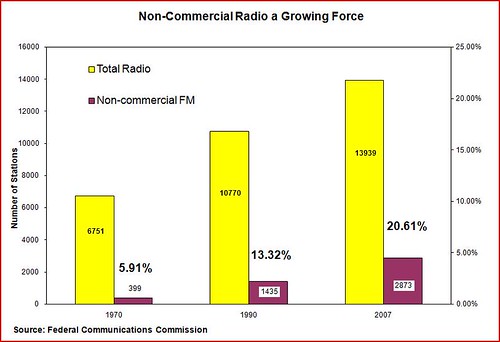

Non-Commercial Broadcast Radio

Terrestrial radio stations don’t just face more competition from each other; they also face a growing non-commercial radio presence. Many surveys of the state of the radio marketplace ignore the impact of non-commercial radio and National Public Radio (NPR) even though it is growing rapidly and capturing listeners from commercial stations. “Non-commercial radio has become a major media force,†notes Ben Compaine of Harvard University.

According to BIA Financial Network, the number of non-commercial radio stations has increased 158% since 1980. And as a percentage of commercial stations, non-commercial stations have grown from less than 6% in 1970 to more than 20% in 2007. Exhibit 4 shows that non-commercial FM radio is now 20% of all radio licenses, up from just 6% in 1970.

Exhibit 4

Just how broad is NPR’s reach today? Check out this blurb from NPR’s, 2005 Annual Report:

“Since its launch in 1970, NPR has evolved into a major media organization, primary news provider and dominant force in American life. In 2005, a record 26 million listeners weekly tuned in to NPR programs. More than 800 public radio stations, throughout all 50 states, bring NPR to their local communities; more than 99 percent of Americans live in an area served by an NPR Member station.â€

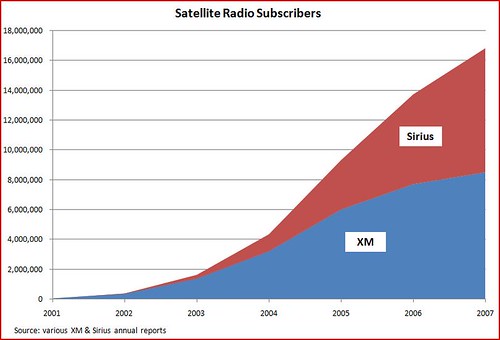

Satellite Radio

Satellite radio, a sector that didn’t even exist before 2001, is now a growing force, too. Subscribership has been growing explosively since 2001. Satellite radio providers XM and Sirius had over 16 million subscribers at the end of 2007, almost twice as many as they had just two years before that. Exhibit 5 documents this growth. Importantly, both satellite radio operators have been stealing away talent from broadcast radio networks and signing other notable media personalities and sports leagues.

Exhibit 5

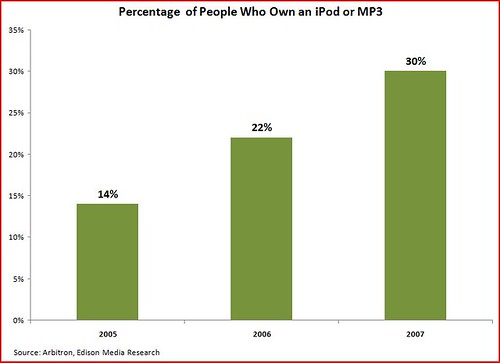

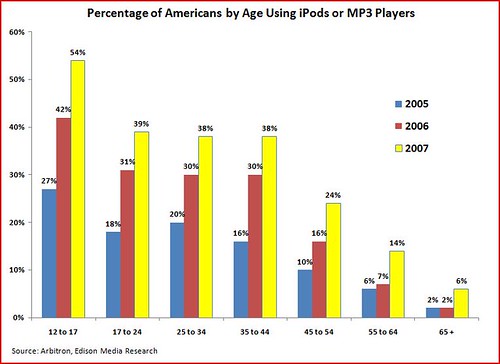

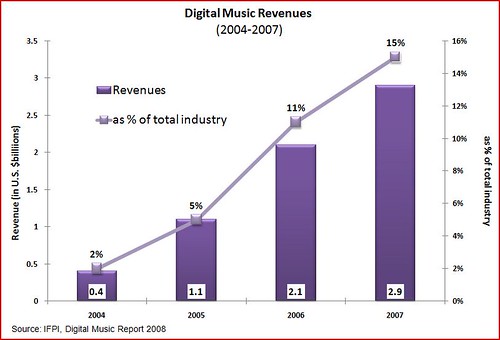

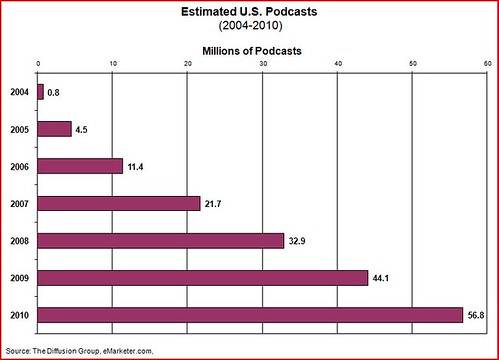

Digital Audio, iPods, & Internet Radio

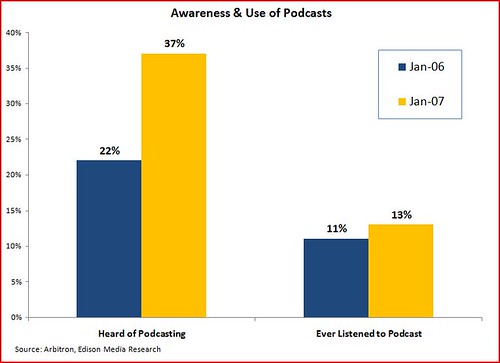

And then there’s the Internet and digital music. New audio competition is rapidly emerging from iPods and MP3 players, online digital music, Internet radio, and podcasting. And now, many of these technologies and services are accessible through our cell phones and other mobile devices (think iPhone and PlayStation Portable, etc.).

Exhibit 6

Exhibit 7

Exhibit 8

Exhibit 9

Exhibit 10

And much, much more is on the way. Sites and technologies like Pandora and Slacker foreshadow a future of hyper-tailored audible entertainment options.

Marketplace Effects

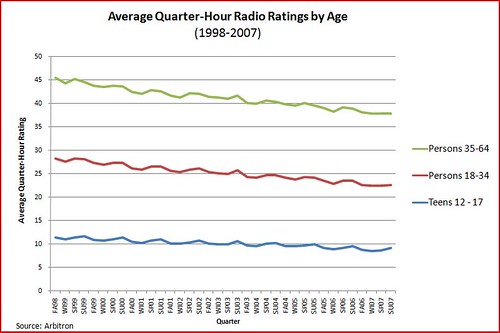

With the rise of new audio competition, broadcast radio station listenership is falling steadily, and is falling fastest for younger demographic groups. According to Arbitron ratings data, from the summer of 1999 to the summer of 2007, average quarter-hour radio ratings for the teen demographic (ages 12-17) fell almost 22%, persons between the ages of 18 and 24 years of age fell by 20%, and persons between the ages of 25 and 35 years of age fell by 18%.

Exhibit 11

Exhibit 12

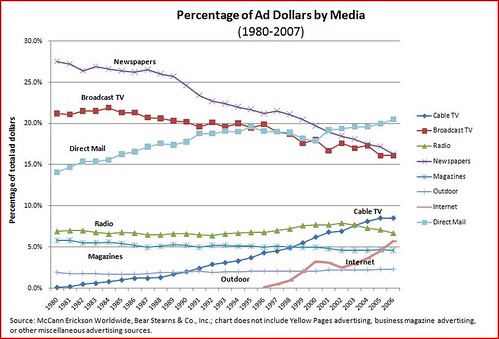

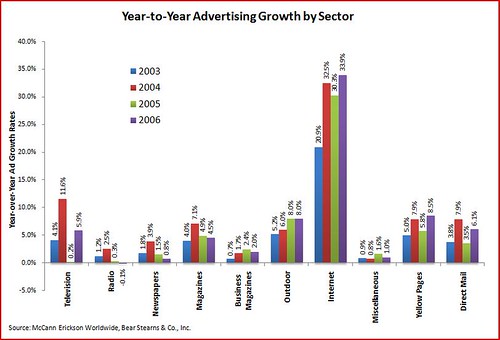

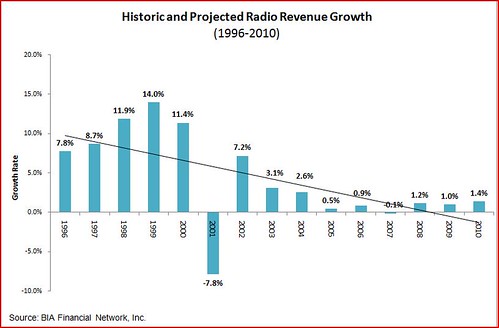

All this new competition for our ears is taking a serious toll on the fortunes of traditional radio broadcasters in particular. As I illustrated in part 3 of the Media Metric series, broadcast radio advertising is starting to drop off significantly.

Exhibit 13

Exhibit 14

Consequently, radio station revenue was down -0.1% in 2007 and BIA Financial Network estimates the radio revenues will not break 1.5% in any of the next three years.

Exhibit 15

What these statistics reveal is that there has never been more cut-throat competition and consumer choice in the world of audible information and entertainment. And things are getting better all the time.