This is the third installment in my ongoing “Media Metrics†series, which aims to evaluate the true state of America’s media marketplace. [See Part 1 for a complete description of the project and the analytical framework I use to research media trends and developments. Part 2 discussed household access to various media technologies]. In this installment, I want to take a look at how various media sectors stack up against each other in terms of advertising support.

You don’t need to have a PhD in media economics to understand the importance of advertising to media companies. “Advertising is the mother's milk of all the mass media,†Wall Street Journal technology columnist Walt Mossberg has noted. And Harold L. Vogel, author of Entertainment Industry Economics, the definitive textbook for media market analysts, has noted that, “Advertising is the key common ingredient in the tactics and strategies of all entertainment and media company business models. Indeed, it might further be said that advertising has substantively subsidized the production and delivery or news and entertainment throughout the last century.†Mossberg agrees, noting that, “Without ads, most editorial products and other programming would be either unavailable or prohibitively expensive.â€

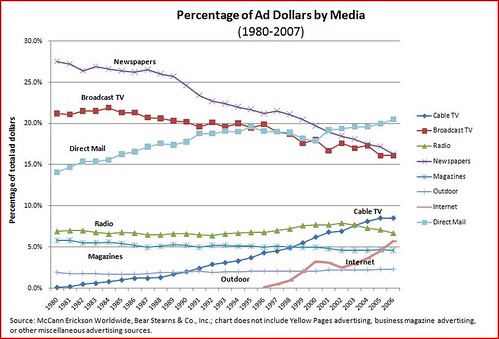

Exhibit 1

More specifically, without ad-supported business models, media operators must rely on either (a) subscription fees / direct sales (when possible), or (b) “charity†in the form of private philanthropy or government subsidy. But, with the exception of “high culture†(opera and art museums) and non-commercial media (NPR, PBS), most media operations in the United States do not rely on philanthropy or government subsidies. Thus, media operators are stuck trying to devise business models that use some combination of subscription fees / direct sales alongside advertising.

This is why economists refer to media sectors as “two-sided marketsâ€; operators have two different sets of “customers†to serve—users / subscribers and advertisers. But, for some media providers, one side of the market—subscribers--cannot be monetized easily or at all. For example, no one has ever come up with a good way to charge for broadcast “over-the-air†television or radio. Similarly, on the other end of the media spectrum, no search engine provider or blogger would succeed very long if they tried to charge people per search or per article read.

This explains why media companies compete so vigorously for advertising dollars; they don’t want to be forced to jack up prices for users / subscribers, assuming it’s even possible to monetize their user base. And in today’s market, advertising competition is more heated than ever before. Exhibit 1 shows how various media sectors stack up against each other in terms of advertising support over the past quarter-century.

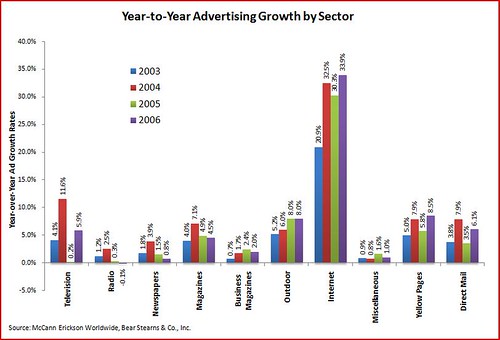

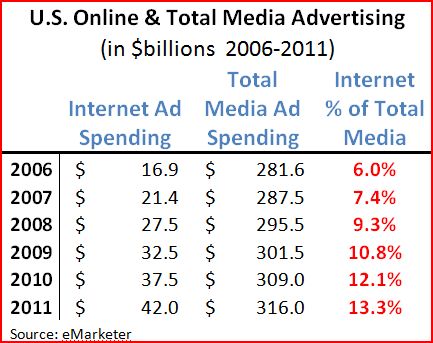

What’s clear is that new media technologies and operators are eating away at traditional media’s advertising revenue streams. In recent years, advertising dollars have been flowing away traditional media outlets (broadcasting and newspapers) and toward cable TV and the Internet. Although other media outlets still garner more advertising dollars, they are quickly losing those dollars to new media players. As Exhibit 2 illustrates, over the past 4 years, Internet advertising has been growing between 20-34% per year while broadcast TV and radio ad revenues have stagnated and newspaper advertising has been falling rapidly.

Exhibit 2

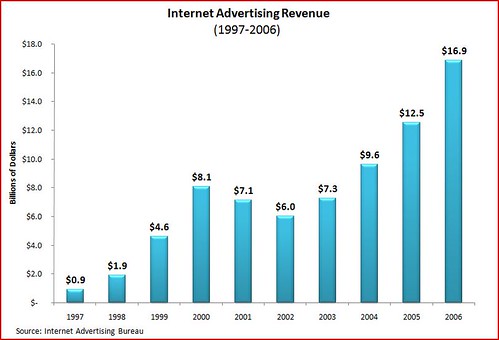

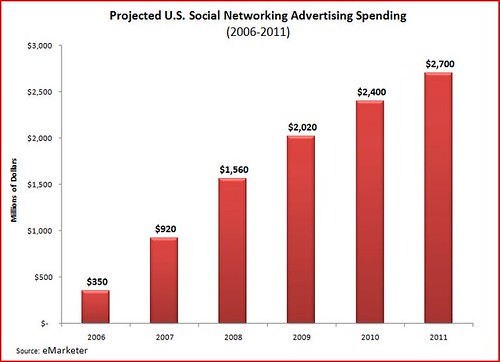

And the situation isn’t going to get any better for traditional media operators as more and more new media options and outlets develop. Exhibit 3 shows the growth of Internet ad spending. Exhibit 4 documents U.S. social networking advertising. And Exhibit 5 provides projections for Internet ad spending over the next five years by U.S. companies.

Exhibit 3

Exhibit 4

Exhibit 5

So, what’s the lesson here? Historically, there has always been a great deal of fungibility or substitutability among media outlets. Advertising support can flow from one media segment to another. And it is doing so today in America’s increasingly dynamic media marketplace. Perhaps the best way to conclude is with this paragraph that appeared in the New York Times Co.’s 2006 Annual Report.

“[C]ompetition has intensified as a result of digital media technologies. Distribution of news, entertainment and other information over the Internet, as well as through cellular phones and other devices, continues to increase in popularity. These technological developments are increasing the number of media choices available to advertisers and audiences. As media audiences fragment, we expect advertisers to allocate a portion of their advertising budgets to nontraditional media, such as Web sites and search engines, which can offer more measurable returns than traditional print media through pay-for-performance and keyword-targeted advertising.†- New York Times Co., 2006 Annual Report

Again, it’s just another sign that America’s modern media marketplace is far more dynamic and competitive than ever before in our history.

[Up next... We'll be examining the changing fortunes of traditional media operators relative to new media and technology companies using a different metric: market cap and other financial variables.]